Newsletters

Quarter 1 • 2026

Rebuild your savings after a withdrawal

At the beginning of March, the two-pot withdrawal period has opened. Some members may have made a withdrawal to deal with debt or unexpected expenses. While withdrawals can help in difficult times, they reduce the money available to you when you retire.

If you have made a withdrawal, now is a good time to start rebuilding your savings.

MORE FROM THIS NEWSLETTER:

Reset your savings goals after a divorce

If a divorce order requires that part of your retirement savings be paid to your former spouse, your total retirement savings can be reduced by a large amount.

This can be discouraging, but it is important to remember that your retirement journey does not end there.

With a clear plan and consistent saving, you can rebuild your savings over time.

Take control of your debt

Debt can build up quickly, especially when unexpected expenses arise. Many members rely on credit cards, store accounts or short-term loans just to get through the month.

Your Fund’s portfolio performance

The chart below shows the investment performance of the Fund’s main investment portfolio – the Balanced Growth Portfolio – over various periods ending 31 December 2025.

Understanding investor behaviour

Markets are not only driven by facts and numbers but also by human behaviour.

When markets rise or fall sharply, investor emotions can influence prices just as much as economic events. It is normal to feel uncertain when markets move quickly or when new events dominate the headlines. At times like these, some investors react emotionally rather than focusing on the long‑term.

Stay focused on the strategy

If your divorce order states that your former spouse must get a share of your retirement savings, this is called a claim against your pension interest. The Fund is required by law to pay the specified amount to the non-member spouse.

Join AF Connect and unlock many benefits

Besides providing easy access to your Benefit Statement, AF Connect has many other benefits. Start taking control of your retirement journey by logging in or registering on AF Connect.

Quarter 4 • 2025

Avoid adding to your debt this festive season

The festive season is the time of year when many members and beneficiaries spend more than they planned, and end up starting the new year with more debt. When money is tight, it is easy to borrow ‘just to get through December’. But every loan or store account you use now will cost you far more in the future. You will also pay interest and often additional fees on the money you borrow. This all adds up and leaves you with less money for your retirement.

MORE FROM THIS NEWSLETTER:

Divorce and your retirement savings

If your divorce order states that your former spouse must get a share of your retirement savings, this is called a claim against your pension interest. The Fund is required by law to pay the specified amount to the non-member spouse.

Small savings add up and build a better future

Many members feel they cannot save because money is tight and debt takes most of their income. The good news is that small steps make a big difference.

Your Fund’s portfolio performance

The chart below shows the investment performance of the Fund’s main investment portfolio – the Balanced Growth Portfolio – over various periods ending 30 September 2025.

Investing in an uncertain world

Investing can feel stressful when markets are unpredictable. The truth is that no one can predict the future, not even experts.

Market update

There was strong growth in South African shares, with a 28.1% return for the year to September 2025.

Quarter 3 • 2025

Update your beneficiaries! Why is it important?

Make sure that your retirement savings, your life assurance and your insurance benefits all go to the right people if you were to pass away while working for Woolworths.

The money that is payable to your beneficiaries is investigated and distributed by the Board of Trustees.

If your beneficiary details are out of date, the trustees may not have clear guidance on exactly who should receive your money.

MORE FROM THIS NEWSLETTER:

Your annual benefit statement has been sent

Your 2025 Benefit Statement has been released via InfoSlips. You should have received an email or an SMS with a link. You can open the link to your Benefit Statement using your ID number.

Withdrawals today, less money tomorrow

What are the negative effects of making a withdrawal from your retirement fund savings?

Your Fund’s portfolio performance

The chart below shows the investment performance of the Fund’s main investment portfolio – the Balanced Growth Portfolio – over various periods ending 30 June 2025.

Respond to global shifts but keep your focus local

Recognising these events helps to explain the ups and downs in your investment statements and highlights why long-term planning remains so important.

Quarter 2 • 2025

Two-pot system overview of claims

In this newsletter, we look at some of the statistics on savings-pot claims since the two-pot system came into effect in September 2024. This can help you understand what choices other members are making and gives a general insight into our retirement fund.

MORE FROM THIS NEWSLETTER:

Pay back your two-pot withdrawals

You should only withdraw from your savings pot if you have a financial emergency – such as having to pay for urgent medical care.

Portfolio performance

Over the long term (seven years or more) the Balanced Growth Portfolio has earned an investment return higher than inflation but has not reached the 5.5% target.

Could USA trade tariffs affect your retirement savings?

Many investors were caught off guard when President Trump announced new trade tariffs and the global stock markets dropped. Their thinking was that Trump would not do anything too foolish and that there would be guardrails in place to soften his strong views on trade deficits. The investors were too optimistic.

Quarter 1 • 2025

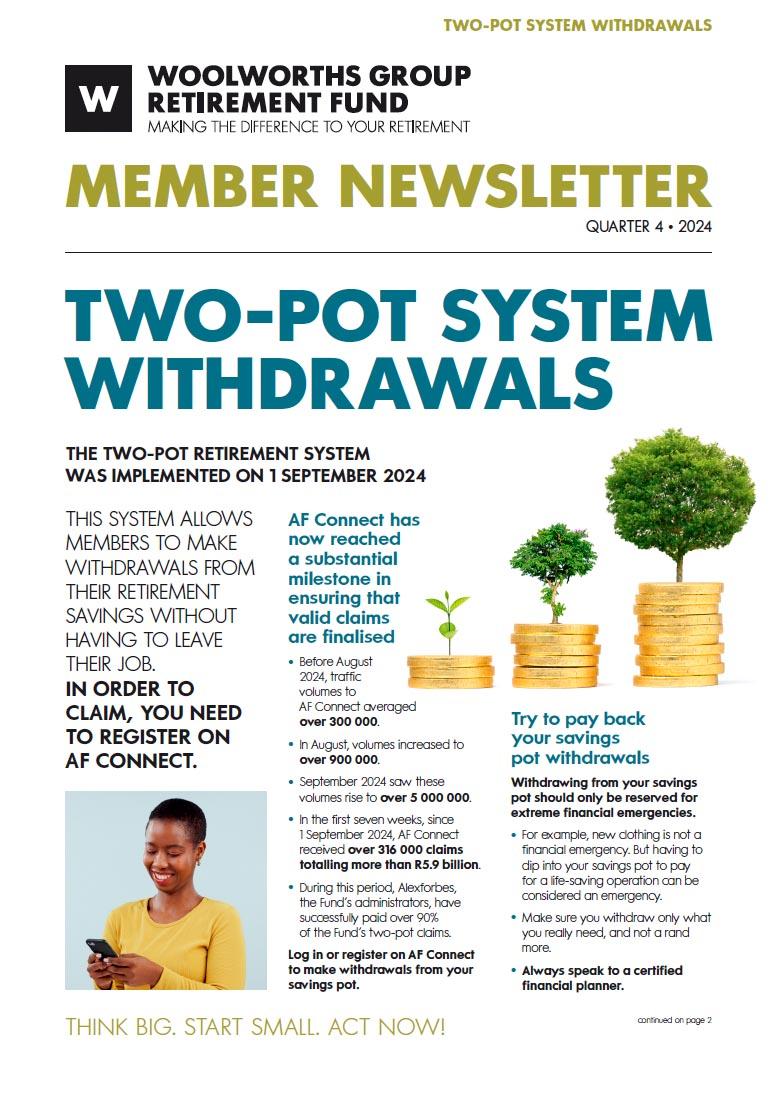

Two-pot system updates

Although the two-pot system was introduced over six months ago (on 1 September 2024), many South Africans still struggle to understand how the new system operates.

MORE FROM THIS NEWSLETTER:

Portfolio performance

Over the long term (seven years or more) the Balanced Growth Portfolio has earned an investment return higher than inflation but has not reached the 5.5% target.

Securing your retirement

Some steps that you can take to secure your retirement. We recommend that you speak to a certified financial planner to help guide you.

Some simple money tips for a better 2025

Some simple money tips for a better 2025 – such as managing your debt and starting an emergency fund, to avoid dipping into your savings if you are in distress.

The impact of the second Trump presidency

Will Trump’s presidency affect global and South African markets? Our article explains why it is difficult to tell.